From 2027-2032, forward power prices are pointing to a decline by a CAGR of -4%

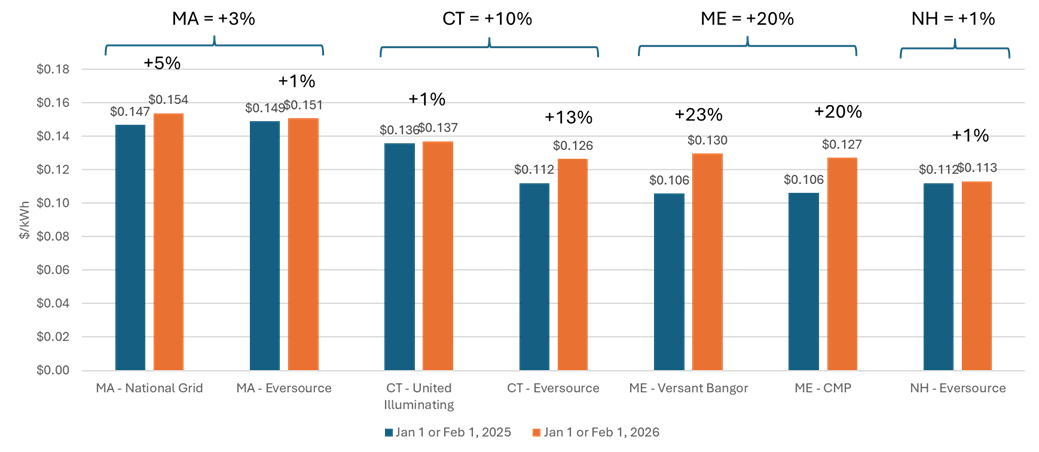

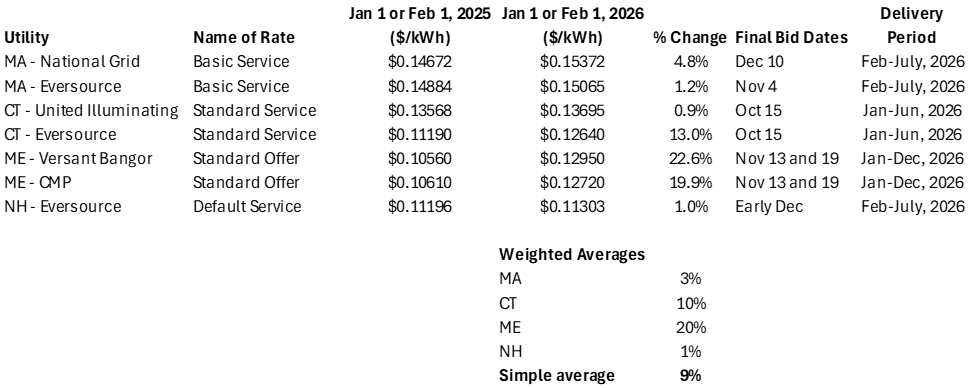

Basic service rates for four New England states are set to move higher in 2026 following recent procurements. The rates for seven utilities across the four states will increase by an average of 9% vs. year-ago levels (see Figure 1). Weighted by load, Massachusetts utilities will increase by 3%, Connecticut by 10%, Maine by 20% and New Hampshire by 1%.

Figure 1. Year Over Year Basic Service Rate Changes ($/kWh)

Source: The utilities

As a result of the increases, owners of community solar or net metering credit projects in these states will see higher payouts per unit of generation. Delivery charges are also a part of compensation, which are not discussed in this article, but are likely to increase as well.

These basic service rate increases are a function of higher wholesale energy prices which in turn are heavily dependent on natural gas prices. Forward natural gas prices were higher and more volatile during the periods when utilities procured supply for 2026, which spanned October 15 to December 10. The key drivers of these prices are global LNG demand, geopolitical risks, and constrained gas infrastructure in New England.

Procurement timing and contract structure

Utilities procure basic service power 1-3 months in advance, and outcomes depend heavily on:

The rates are different from utility to utility because of procurement specific reasons including the following:

While basic service rates are primarily based on the commodity itself, wholesale prices increasingly reflect:

Suppliers price these risks into bids, especially for longer-term commitments.

The changes for 2026 are slightly more moderate than prior years where rates have zig zagged dramatically up and down.

Unlike other ISOs such as PJM and MISO, New England hasn’t yet been exposed to a run up in capacity prices. That’s because the New England capacity auction calls for capacity with a 3 year advance window.

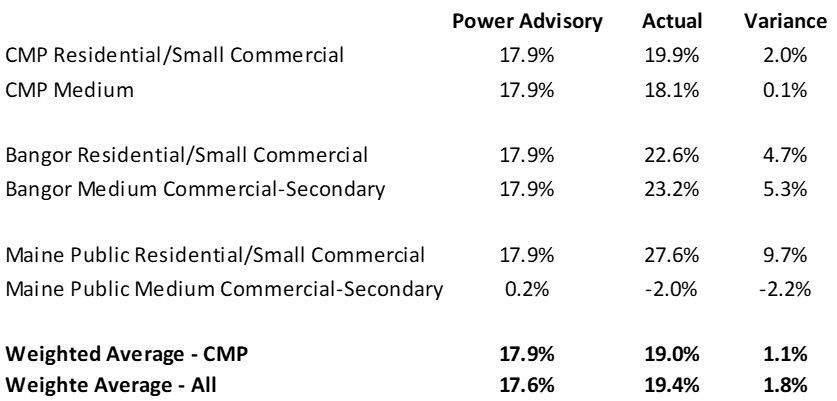

Power Advisory Maine estimates

Power Advisory’s estimates of these new rates was quite accurate. Using Maine as an example (Figure 2), our estimates were just slightly above where rates actually came in.

Figure 2. Variance vs. Actual Year-over-Year Increases for Maine Standard Offer Rates

Forward prices pointing to declines

Following the 2026 year, forward prices in New England are pointing to a 5-year CAGR of -4.4% with virtually no variation at all among load zones (+/- 0.1%). Thus, based on current trading of delivery of future power contracts and longer term expectations, these basic service charges are expected to decline. Some of the reasons for this include:

Andrew Kinross can be reached at akinross@poweradvisoryllc.com.