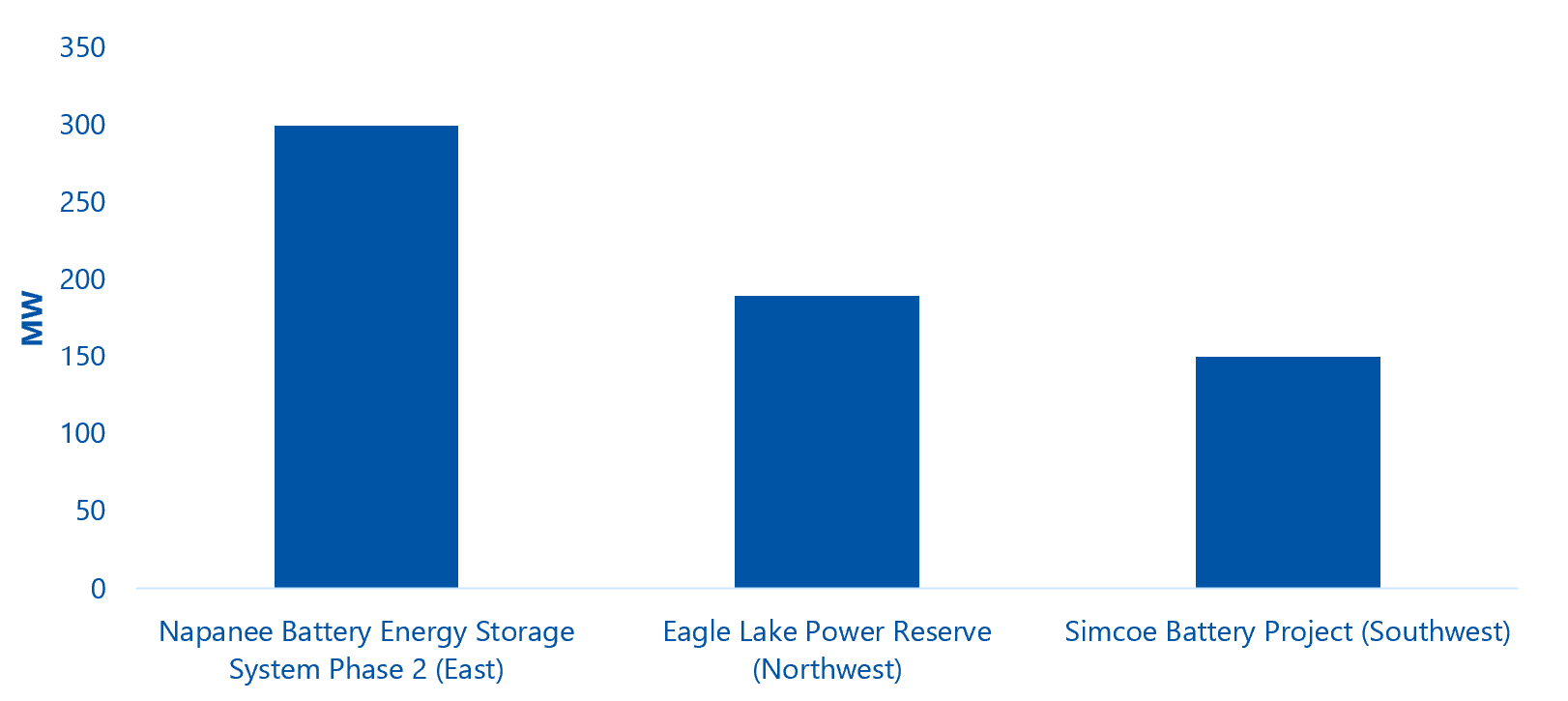

The Independent Electricity System Operator (IESO) released the initial results from its Long-Term 2 capacity stream window 1 (LT2(c-1) – announcing that it had procured 640 MW of capacity from three 8-hour Battery Energy Storage Systems (BESS). Notably, the only successful participants were BESS systems, even though the procurement was open to both BESS and gas-fired generation. The total target capacity for the procurement was 600 MW.The weighted average price of the contracts is $563.58/MW-Business Day or around $140/kW-Year (excluding market revenues).In terms of location, the procured assets are dispersed across the province, with the largest asset (300 MW) located in the East zone in Napanee. The other two projects – 190 MW and 150 MW – are located in the Northwest and Southwest zones, respectively.

Power Advisory Commentary

The results of the LT(c-1) are interesting for a few reasons:

1. Long Duration BESS Cost Competitive with Gas-Fired Generation– With 8-hour BESS accounting for the only successful projects, the procurement shows that BESS is increasingly a cost-competitive source of capacity compared to traditional gas-fired generation. It should be noted that BESS assets qualify for the Investment Tax Credit (ITC), which can lower the project’s up-front capital costs by up to 30%. As such, policy levers such as the ITC are helping to support the competitiveness of BESS assets compared to gas-fired generation.

2. BESS Costs Continue to Decline – The procurement results also highlight the ongoing cost decline in BESS assets through repeated procurements. The contract price in $/MW-Business Day has declined by nearly 50% from the E-LT procurement in 2023 and more than 16% since the LT1 procurement in 2024. As noted, part of that decline can be attributed to the ITC, while a drop in component costs is likely also helping to reduce installed capacity costs (and bids). More competitive auctions (i.e. more participants) may also support lower bids. Some bidders may also be taking a more aggressive view of market revenues, based on the higher prices in the renewed market since it launched in 2025 and ongoing forecasts for a tighter supply/demand balance in Ontario. A more aggressive view on market revenues can help lower the capacity bid submitted in the procurement, as more revenues to support the project will come from merchant exposure in the wholesale market.

3. What Comes Next for Gas-Fired Generation? – The IESO has publicly stated that it will likely require new gas-fired generation to meet future reliability needs. While long-duration BESS assets (i.e. 8-hours or longer) may act as a replacement form of capacity, the value of that capacity will decline as more BESS assets are added to the grid. At its most basic, the Effective Load Carrying Capacity (ELCC) – which is a measure of how much a resource’s installed capacity can be expected to be available during peak demand hours – will continue to decline as more BESS is procured and added to the grid. At some point, the IESO may specifically need to procure gas-fired generation for reliability purposes, even if the cost of that capacity is greater than BESS capacity. We expect future Annual Planning Outlooks (APOs) or other reliability-related analyses from the IESO to discuss this issue.