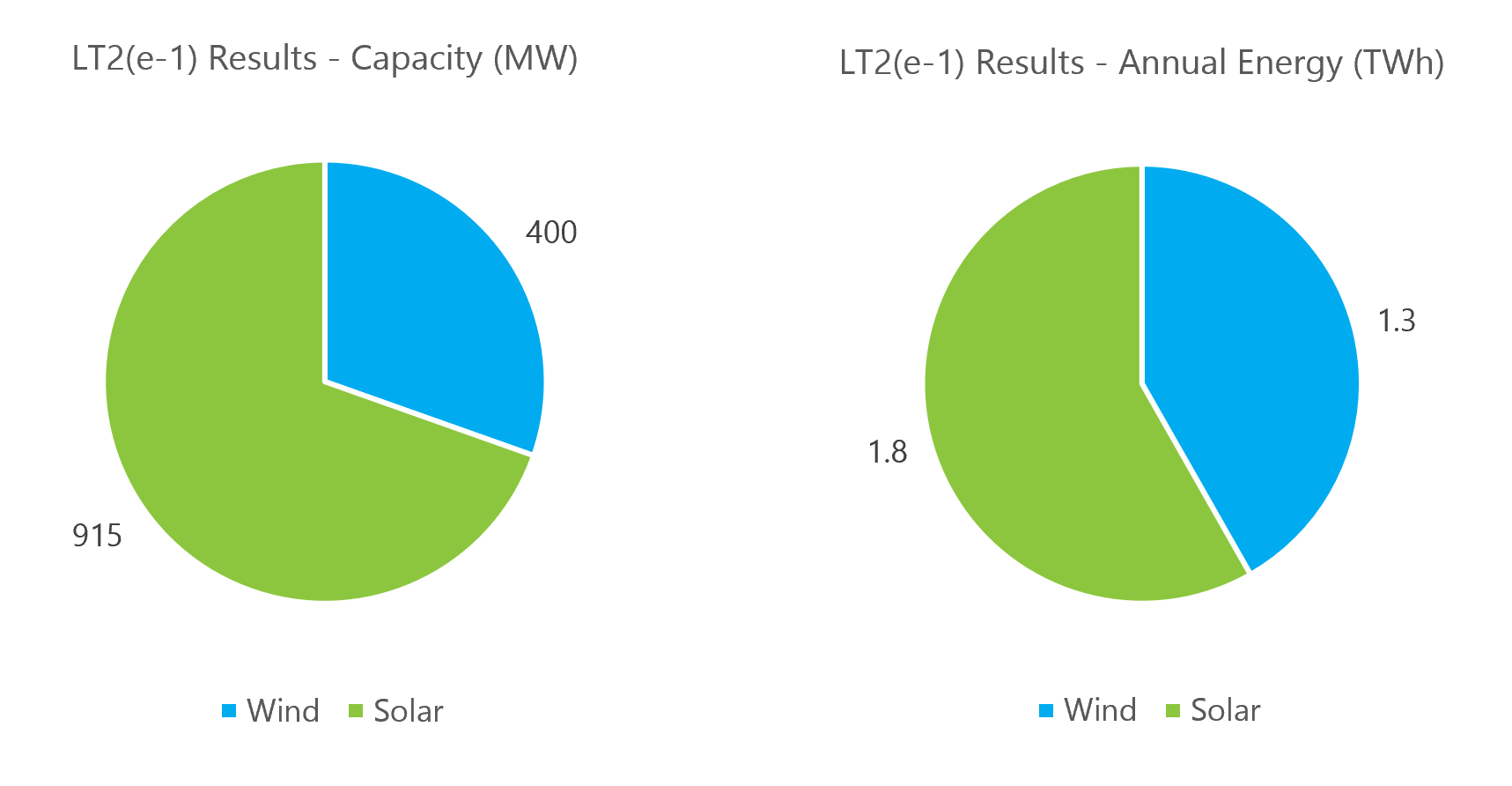

The Independent Electricity System Operator (IESO) released initial results from the Long-Term 2 energy stream window 1 (LT2(e-1) - 1,315 MW of wind and solar resources. Wind power accounted for 400 MW procured, while solar resources accounted for 915 MW – or 30% and 70%, respectively, of total capacity procured. On an annual energy basis, the procurement will provide ~3 TWh of annual energy – roughly the target capacity in the procurement – when all of the projects are operational. The split between the two resources procured on an annual energy basis is closer at ~1.3 TWh for wind and ~1.8 TWh for solar, a 40% and 60% split respectively.The weighted average price of the contracts is $87.80/MWh.

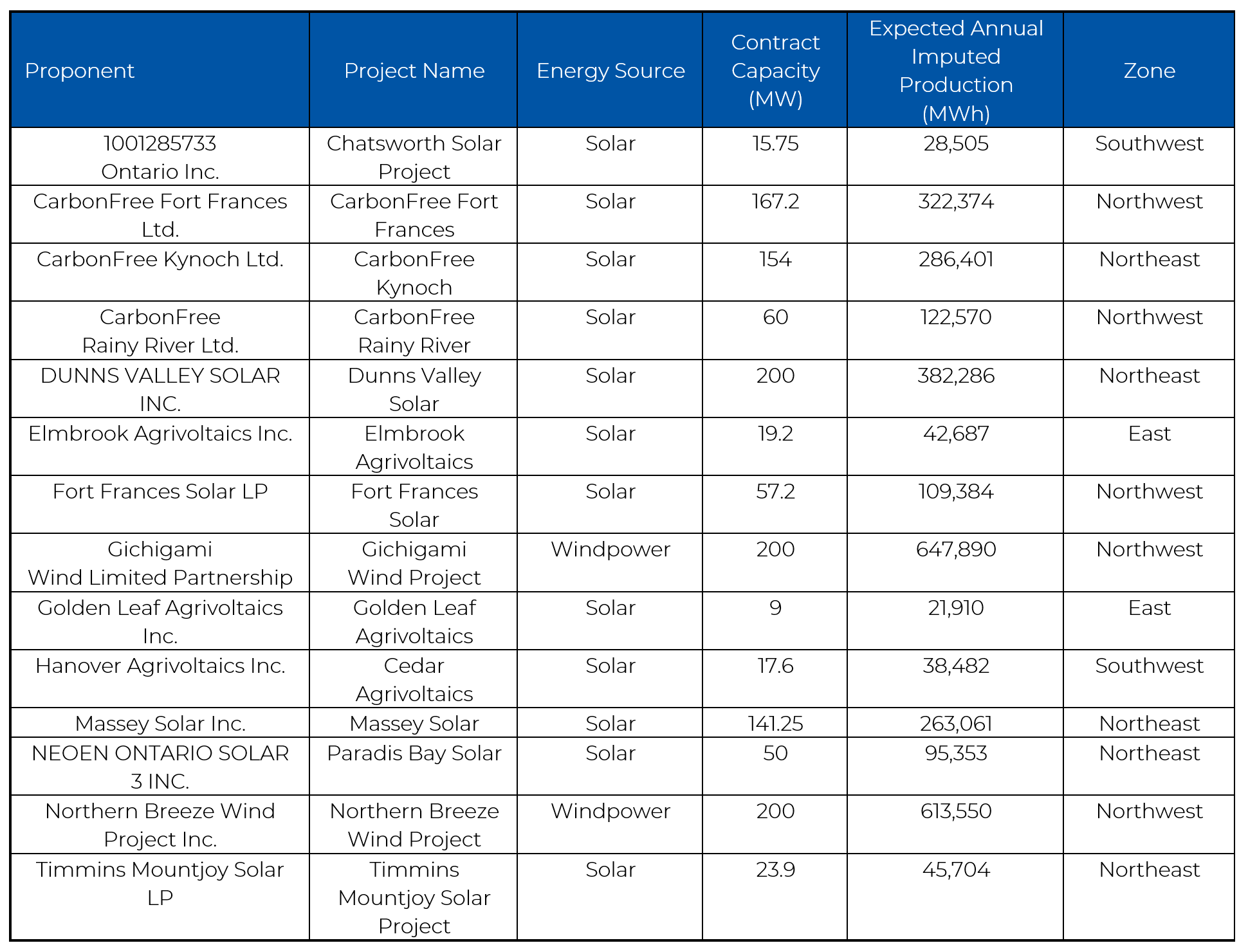

All of the projects procured had at least 50% indigenous participation, which provided additional points in the scoring of the different projects.

In terms of location, the procurement was heavily tilted to both the Northwest and Northeast Zones. In total, the two northern zones accounted for 1,253 MW or 95% of the total MWs procured. The only projects located in the southern zones were solar projects – all less than 20 MW – in the East and Southwest electricity zones.

Power Advisory Commentary

The results of the LT(e-1) met the overall targets of the IESO, which was for 3 TWh of energy and represents progress for the IESO on evolving procurement process for future LT2 windows, among other procurements in the future. Nonetheless, we have a few comments:

1. Solar projects dominate – while we expected some solar projects to be successful, the 60/40 split in terms of annual energy for solar compared to wind was higher than we expected. How this energy impacts future market operations will be intriguing as the power system expands and demand grows.

2. Siting is hard to do – as expected, many of the projects – and both the two large wind projects – were sited in the Northwest and Northeast zones. This highlights the challenges of siting projects, particularly large wind projects, in the southern zones that are closer to the major load centres. The IESO is currently moving forward with multiple transmission projects across the Northwest and Northeast zones that will facilitate moving that energy around the northern zones to meet forecasted demand growth as well as transfer to the southern load centers. The Minister of Energy and Mines – on advice from the IESO – has identified as a priority project a significant transmission expansion from northern zones to the south1, which will further alleviate congestion. If future procurements continue to focus on the Northeast and Northwest zones, these transmission investments will be even more critical.

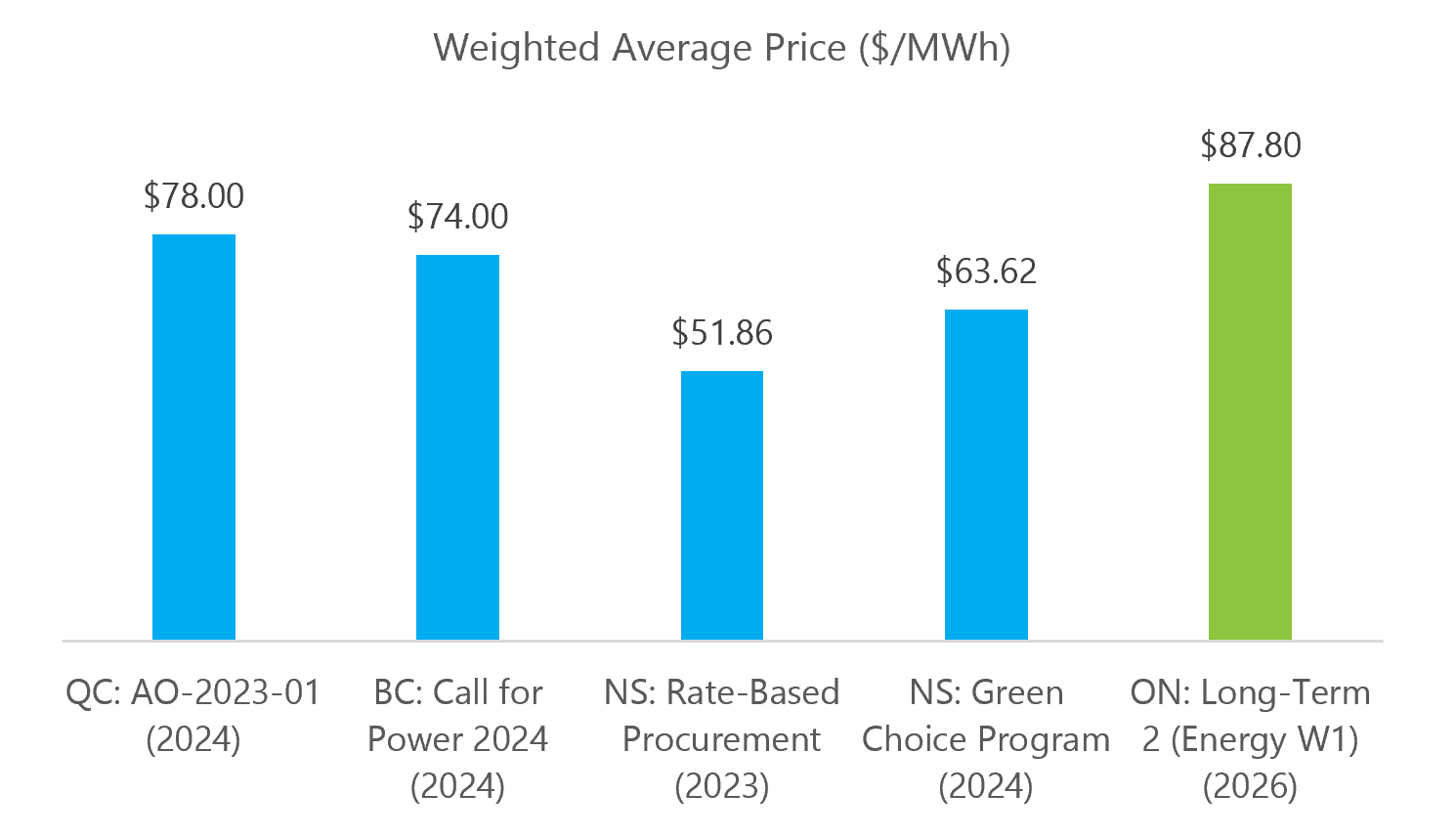

3. Energy Price Comparison – the weighted average price of $87/MWh – which includes the Investment Tax Credit – is higher than recent procurements across Canada for renewables (see chart below). The higher price could be explained by challenges outside of the control of proponents and the IESO (e.g., global trade tensions, geopolitical risks) but consideration should be given to the siting restrictions, municipal support resolution requirements, deliverability threshold, and compensation approach of the LT2(e-1) RFP and contract. Each aspect would influence proponent risk-analysis and ultimately bid price. We note that the weighted average price reported by the IESO is close to the lower end of the range of prices we developed based on our own internal modelling last fall.

4. Future Deliverability – the award group in LT2(e-1) will impact the deliverability of future energy (and capacity) windows for LT2. Growing load expectations and new transmission expansions should expand the deliverability options, but with so much new supply awarded in northern Ontario, it is reasonable to consider how much remaining deliverability there will be.

<1> Order-In-Council 1661/2025 - https://www.ontario.ca/orders-in-council/oc-16612025