On March 16, 2026, Massachusetts Governor Maura Healey introduced an Executive Order that establishes a target of 10 GW of new energy supply-side and demand-side resources over the next 10 years, alongside as separate goal of 5 GW of energy storage. The 10 GW target includes:

• 4.0 GW of new in-state solar

• 3.5 GW of new electric demand reduction to be achieved through load management strategies such as energy efficiency, virtual power plants, and electric vehicle charging management

• 2.5 GW of new energy supply delivered to the New England grid connected to Massachusetts.

The order also establishes a 15-month limit for final state and local permitting decisions on large-scale infrastructure. The process will be overseen by a newly created Energy Infrastructure Siting and Permitting Council, which has yet to be established. This streamlined approach will be a welcome relief to developers who often take 2-3 or more years to navigate the process.

In parallel, comprehensive energy legislation is advancing through the State legislature. On Feb 26, 2026, the House approved H.5175, a bill focused on energy affordability, clean power and economic competitiveness, which includes a requirement of 10 GW total installed base of solar by 2040. The bill still needs Senate and Governor approval.

If passed, the bill would likely guide or dictate to some degree the implementation of the solar build out. In the current bill, it suggests that a commonly understood framework be used for the solar program such as an “adjustable block incentive, a competitive procurement model, tariff or other declining incentive framework”. It also specifies that the program should: “promote investor confidence through long-term incentive revenue certainty and market stability”. These principals have historically underpinned Massachusetts solar programs and will likely be viewed favorably by market participants.

Federal ITC Phaseout Creates Urgency

To qualify for the Investment Tax Credit (ITC), solar projects must:

• Begin construction by July 4,2026, or

• If construction begins later,be placed in service by December 31, 2027

This structure creates a narrowing development window. Projects that meet the construction start deadline benefit from more flexible completion timelines, while those that do not face a hard placed-in-service cutoff.

The Executive Order emphasizes the need to take immediate action in order to maximize the federal tax credits that clean energy projects in Massachusetts are eligible to receive prior to their expiration.

After the ITC phases out, the cost of developing solar projects is expected to rise. This raises an important policy question: how will expanded state incentives be balanced against growing concerns around electricity affordability?

The Evolution of Solar in Massachusetts

According to the Solar Energy Industries Association (SEIA), Massachusetts has 5,775 MWDC of solar online. Massachusetts is by far the largest solar state in New England and is about equal in size to New Jersey, which is the largest solar state in all of PJM.

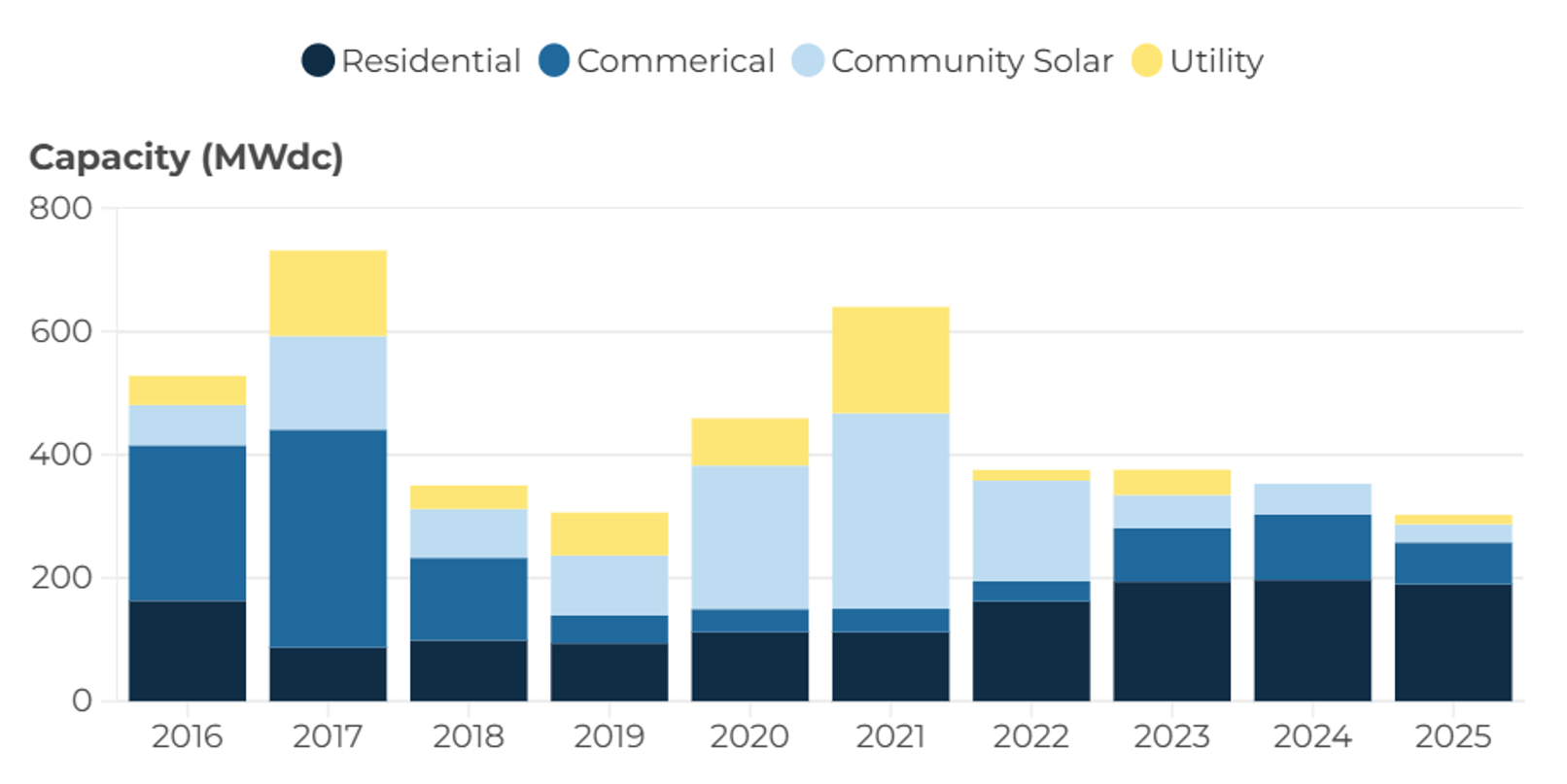

Despite some starts and stops during program reviews, the Massachusetts market has been a very reliable and consistent solar market. Politicians have been supportive of industry, and the Massachusetts Department of Energy Resources has consistently made improvements to the program when necessary. Over the past ten years, annual installations have been running about 400 MW on average (Figure 1). For the five years prior to that, this was in the 200-300 MW per year range. The SREC 1 program was introduced in 2011, and SREC 2 in 2015. The SMART program was introduced in 2018, and has been the main driver of installations since then. A robust net metering program has also been responsible for development of hundreds of megawatts.

Figure 1. Annual Massachusetts Installations by Project Category, Last 10 Years

Assuming that the 4 GW of solar is added from now through 2035, that would amount to 400 MW per year, a continuation of the market size over the past 10 years. In recent years, the residential market has accounted for the largest part of installations. The new bill would support all project categories.

Market Leaders

The Massachusetts market is a fragmented market with dozens of developers and project owners. The largest current project owners are shown in Figure 2. These are comprised of large national players and smaller regional players.

Figure 2. Leading Owners of Massachusetts Solar

While the program design will be key to the economics of commercial and utility scale projects, all signals point to a robust continuation of the Massachusetts market while there remains significant uncertainty elsewhere in the country.

Andrew Kinross can be reached at akinross@poweradvisoryllc.com.