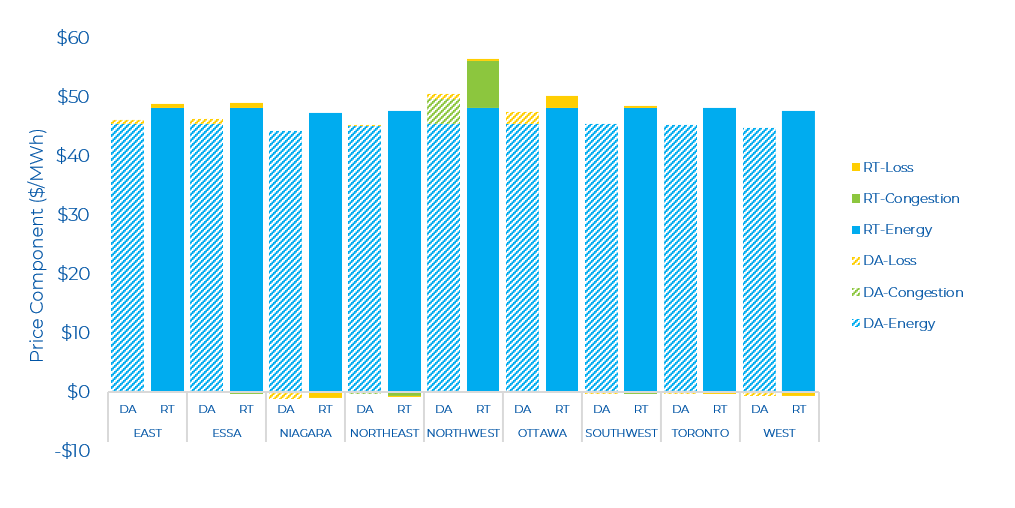

Day-Ahead and Real-Time Price Trends by Components and by Zone

The wholesale market in Ontario – and wholesale markets across the Eastern seaboard – have taken a breather. The average Day-Ahead (DA) dropped to $46/MWh compared to $117/MWh in February. DA zonal prices ranged from $43/MWh (Niagara) to $51/MWh (Northwest), while Real-Time (RT) zonal prices ranged between $47/MWh (Niagara) to $57/MWh (Northwest). In contrast to previous months (since November), the Ottawa zone was no longer the highest priced zone in both the DA and RT markets. This is likely to do with the milder weather last month compared to the previous months and more moderate exports from the Ottawa zone to Quebec.

The DA and RT price by zone and by component for the past month is shown below. Prices in the Northwest zone were higher because of increased congestion.

Day-Ahead and Real-Time Prices

The number of very high prices in February significantly declined in March. However, general volatility continued with 21 real-time hourly OZP spikes greater than $200/MWh. As noted, the average hourly day-ahead OZP was $45.85/MWh in March, while the real-time OZP was $48.83/MWh. The highest real-time OZP was $581.32/MWh (on March 31, HE 20). The peak Ontario demand in March hit 20,395 MW (on March 2, HE 19). The March Ontario peak demand was 1,206 MW lower than the peak in February – again, a result of more moderate temperatures. The Ontario demand on March 31, HE 20 – when OZP hit its highest level – was 17,776 MW, which is well below the peak demand of more than 24,000 MW in the summer of 2025.

OR Prices

There were fewer real-time Operating Reserve (OR) price spikes in March compared to February. Similarly, March observed low day-ahead and real-time average monthly OR prices. The day-ahead OR price was the lowest since the launch of the renewed market. The real-time OR price was a bit higher than the prices observed in August and September of last year. The average monthly day-ahead 10S price was $3.39/MWh, while it was $10.35/MWh in real-time. The DA OR price was more in line with historical averages in the legacy market. The highest real-time OR price spike of $484.98/MWh occurred at the same hour as the highest real-time OZP spike. In the day-ahead market, the most common 10S price was $0/MWh (occurred 72% of the time) while in the real-time market, it was $0.10/MWh (occurred 16% of the time).

The highest day-ahead OR price was $112.83/MWh, which occurred on March 24, HE 19. The day-ahead energy price was $75.66/MWh at this time. The day-ahead OR price exceeded the day-ahead energy price in 10 hours in March. This trend is significantly lower than the amount in February, where 53 hours experienced the OR price exceeding the energy price – meaning that in these hours the OR market was tight and reserve prices can put upward pressure on energy prices due to co-optimization. The previous tightness that occurred in the reserve market was not observed last month.

Real-time OR prices were low (i.e., near $0.10/MWh) for many hours. There were several hours with real-time OR price spikes, coincident with real time OZP spikes. The highest real-time OR price was $484.98/MWh on March 31, HE 20. The real-time OR prices exceeded the real-time energy prices across 9 hours in March. This is lower compared to February when there were 26 hours when OR prices exceeded the energy prices.

Zonal Prices and Congestion

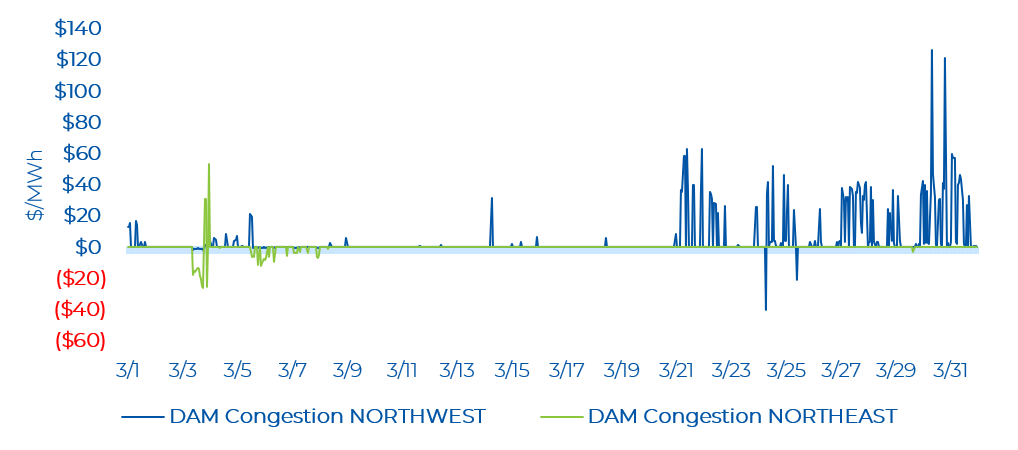

In March, there was no congestion across most zones. The only zones that showed congestion were the Northwest zone and the Northeast zone. The Northwest zone saw a high of $126.97/MWh and low of - $40.30/MWh. Most of the congestion for this zone was positive and concentrated in the end of the month. The Northeast zone saw a few hours of negative and positive congestion with a high of $53.47/MWh and low of - $26.28/MWh. Note that negative congestion typically means there was a constraint exporting energy from a particular zone (and lower energy prices), while positive congestion is the opposite.

In real-time, the Northwest zone saw several hours of consecutive positive congestion, especially concentrated in the end of March. The Northwest zone saw a high of $562.40/MWh (on March 26, HE 21) and a low of - $177.24/MWh (on March 23, HE 22). The Northeast zone saw mainly negative congestion with a high of $60.16/MWh (March 29, HE 10) and a low of - $62.70/MWh (on March 3, HE 16).

In March, there were several outages on the East-West Transfer East (EWTE)/East-West Transfer West (EWTW) interfaces, which can limit flows between the Northwest and the rest of the province and cause significant congestion. There continues to be reduced capacity maintained on Flow-South (FS) (FS is operating at minimum capacity) for all of March, since December. Again, this can limit the flow of energy from the northern zones to the major load centres in the south. There was also some reduced capacity on the Virtual Trading Northeast Zonal Limit and outages on other interfaces: Flow East to Toronto (FETT), Transfer East of Mackenzie, Transfer East of Kenora, St. Lawrence West, Ontario-Michigan Import and Export and Ontario-Minnesota Transfer North (MPFN). There was minimal reduced capacity on the Flow Into Ottawa (FIO) and the Ontario-Quebec Beauharnois Import (ON-QC Beauharnois) interfaces compared to what was observed in the previous months.

Other than the Northern zones, in real time, the West saw minimal congestion. The West zone experienced a high of $40.31/MWh and a low of -$117.60/MWh.

In March, the number of congested hours in the Northern zones remain relatively high (although has dropped for the Northeast zone compared to February). However, the number of congested hours has significantly dropped for all other zones.

As shown in the figure below, similar to February, March saw many northern major interfaces with reduced capacity, specifically the EWTE/EWTW and FS. The FIO and ON-QC Beauharnois interfaces had relatively low occurrences of reduced capacity in March. The occurrence of reduced capacity on these outages was often connected to the extreme weather conditions experienced in these winter months.