The second full week of the post-Market Renewal Program (MRP) has passed and a number of trends from the first week remained in place.

As noted in our first weekly review, MRP is still very much in its early stages and it is not clear whether some of the trends that we are seeing are long-standing or part of the “growing pains” process of a new market. Also, as noted last week, the spring shoulder season introduces some unique conditions on the electricity grid – namely that many of the province’s hydroelectric facilities move to “must run” operations and exit the Operating Reserve (OR) market – that will end in the next month, or so. Demand in the shoulder season is moderate and we have yet to see the new, post-MRP market operate through peak demand conditions. Nonetheless, the early data from the post-MRP market show a more volatile market in real-time with much higher OR prices (in both day-ahead and real-time).

Price Volatility in the Real-Time Market Has Been a Regular Occurrence

The volatility in real-time prices that we saw in the first week has carried over into Week 2. Nearly every day the real-time hourly Ontario Zonal Price (OZP) moved higher than $100/MWh, which is well above the marginal cost of a typical thermal resource in Ontario. The OZP is a load-weighted average of all Locational Marginal Prices (LPMs) in Ontario. In total, there were 19 hours where the price was greater than $100/MWh last week, compared to 8 in the first week in May and 0 hours in the equivalent week in 2024 when the uniform price was still determined by the Hourly Ontario Energy Price (HOEP). The highest real-time OZP was nearly $800/MWh – which would typically be a signal for scarcity conditions facing the grid (discussed in more detail below).

The day-ahead OZP continued to be much more moderate compared to the real-time OZP – with the day-ahead OZP averaging $19/MWh for the week, compared to $38/MWh in real-time.

OR Prices Remain Elevated

Similar to the first week, the post-MRP OR market has experienced significantly high prices and volatility. Interestingly, the high prices have occurred in both the day-ahead and real-time markets. The day-ahead OR price at the Richview Reference node for 10S averaged $23/MW, while the real-time price for the same product was $54/MW. In both cases, the OR price was above the OZP. In Hour Ending (HE) 8 on May 11th, the real-time OR price hit $600/MW, which is one of the prices included in the IESO’s new Operating Reserve Demand Curve (ORDC). The ORDC is an administrative price used when there is a shortage of OR offers. In the legacy market the IESO used a voltage reduction offer in the OR supply stack.

Short-Term OR Divergence or Structural Change?

The major question around OR prices in the post-MRP market is two-fold. First, is this a short-term phenomenon that will be resolved when we move through the shoulder season and freshet (i.e. the “must-run” conditions facing many hydroelectric facilities) and into more “normal” operating conditions? Second, is this structurally any different than the type of pricing we experienced under the legacy IESO-Administered Market (IAM)?

The answer to the first question is hard to say with any confidence. But the answer to it largely ties into the answer to the second question. Ontario experiences freshet every year (i.e. this is a normal feature of Ontario’s grid and is no way connected to broader market design changes) and it is useful to look at how historical prices compared to OR prices under the post-MRP market, as well as what prices looked like in the run-up to MRP implementation.

Looking back to 2021, 10S OR prices in the first two weeks of May ranged from $6/MW (2024) to $19/MW in 2022. In the first two weeks of 2025, the average real-time OR price has been $51/MW, while the day-ahead price has been $30/MW. These prices are materially higher than what we have seen in the previous 4 years.

If we look at the run-up to MRP, we also see materially different prices. The following figure shows the price of 10S OR in the week prior to MRP compared to the two-weeks since it was launched. There appears to be a structural change (for now) between the price of OR before and after MRP was implemented. Again – as we have highlighted throughout our commentary – MRP is still in its infancy and these outcomes may change as bids/offers are adjusted and the scheduling and dispatch of OR resources evolve. Nonetheless, what we have been seeing the first two weeks does not line up with prices prior to MRP’s implementation.

And it is not simply a real-time outcome. If we look at 10S prior to MRP and day-ahead 10s (post MRP), we get a similar result.

Nodal Prices Diverge Across the IESO-Administered Market

The introduction of LMPs was expected to send a more accurate picture of the price/value of energy at different points on the grid (i.e. highlight the impact of congestion and transmission losses). As we said prior to MRP launching, we expected that prices in the Northeast and Northwest zones would likely experience much higher congestion and transmission losses than nodes across southern Ontario. In our commentary last week, we showed that this has been the case, with prices moving lower as you move into the Northeast and then into the Northwest zones.

What is interesting is that the spread in nodes is much greater in real-time than in day-ahead. The following graph shows the average price of the more than 900 different nodes in the first two weeks of MRP. While a majority of the nodes are broadly aligned (most nodes across southern Ontario) there are a number of nodes that above or below the majority of prices. In short, your node matters when it comes to energy prices (and revenues).

Interestingly, there are few nodes – particularly in the Northwest – where prices are below average in the DAM and well above average in real-time.

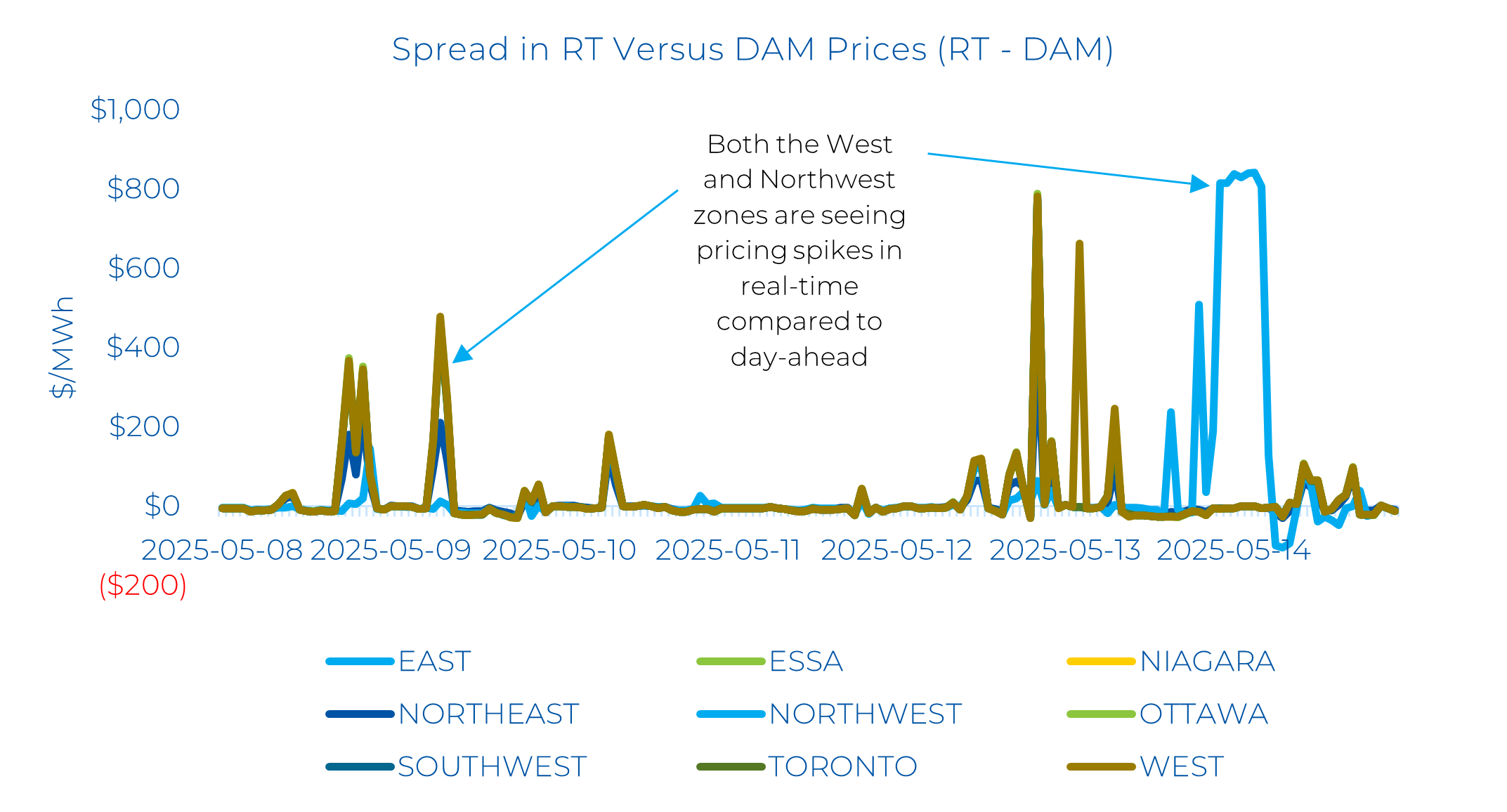

Northwest Zone Experiencing Extreme Volatility

The nodal spread that we have seen at a number of nodes in the Northwest highlights the general volatility that the region experienced over the past week.

The only other zone that has something similar is the West zone where real-time prices have been much higher than day-ahead.

The Impact of a Nuclear Outage on Real-time Prices

In many respects, Ontario has a unique supply mix. The province is home to more than 12,000 MW of nuclear capacity, which typically runs as a baseload resource and operates on a 24/7 basis through the year. Given the size of nuclear units and their proportion of total supply, an outage between day-ahead and real-time would be expected to have a material impact on real-time prices. We had our first experience with a nuclear outage last week, as three units at the Bruce Nuclear Generating Station (“Bruce”) were de-rated (they did not go fully offline) beginning in HE 21. Real-time prices on a 5-minute basis across numerous zones in southern Ontario hit the price ceiling of $2,000/MWh. Overall, the real-time OZP hit $778/MWh. High real-time prices can act as a payment from under-performing generators to over-performing generators compared to their day-ahead schedule. For example, gas and hydroelectric generators that were capable of increasing their real-time supply would have earned additional revenue, while the Bruce units would have to “buy back” their day-ahead schedule at very high real-time prices. The day-ahead price for the same hour was around $50/MWh, meaning the Bruce units would have had to pay hundreds of dollars per MWh for every shortfall of supply in real-time. Additionally, if the load forecast for non-dispatchable loads, such as Local Distribution Companies (LDCs) in day-ahead was lower than their actual consumption in real-time, they would have to purchase the additional energy at the real-time price. This spread is what will make up the Load Forecast Deviation Adjustment (LFDA).

Stay Tuned

Power Advisory’s analysis of the post-MRP will continue to evolve as more data becomes available and more information is released. While there is a significant amount of data provided by MRP, there continue to be a number of uncertainties that we are investigating. If your organization has questions, please do reach out to the Power Advisory team.