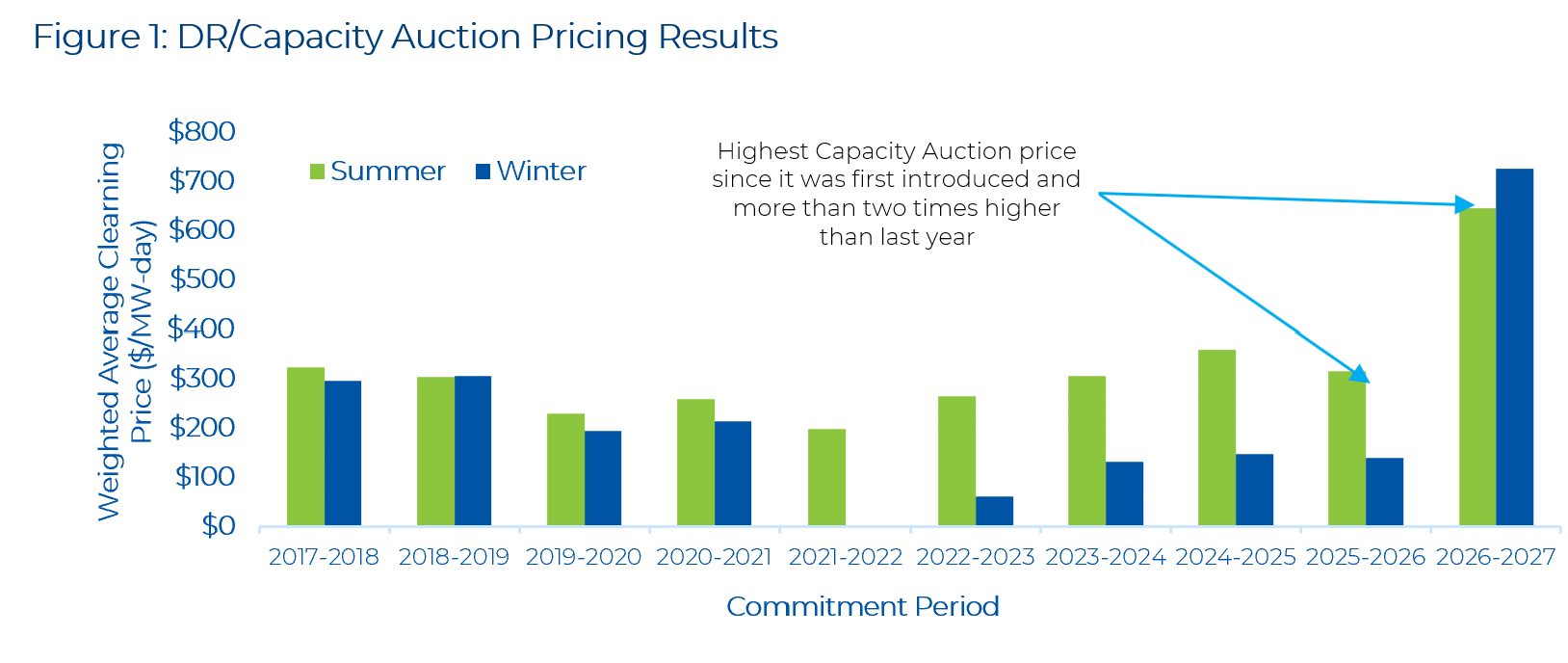

On December 4, 2025, the Independent Electricity System Operator (IESO) released results from its annual Capacity Auction with a summer and winter clearing price of $645.24/MW-day and $725.31/MW-day, respectively – marking the highest ever clearing price in Ontario for the Capacity Auction and a significant jump from the $332.39/MW-day and $139.00/MW-day for the summer and winter in last year’s auction.

The winter clearing price, in particular, was higher than the IESO’s reference price, which is an indicative value of the cost of capacity – currently based on a gas plant – and is used to determine the maximum clearing price. The higher price of capacity – now higher than the IESO’s estimate of the cost of capacity in the winter – is a further sign of the tightening supply/demand balance in Ontario. In contrast to the last two auctions, the summer CA prices in the Northwest and Northeast zones were the same as other zones – meaning there was no longer a locational spread in clearing prices.

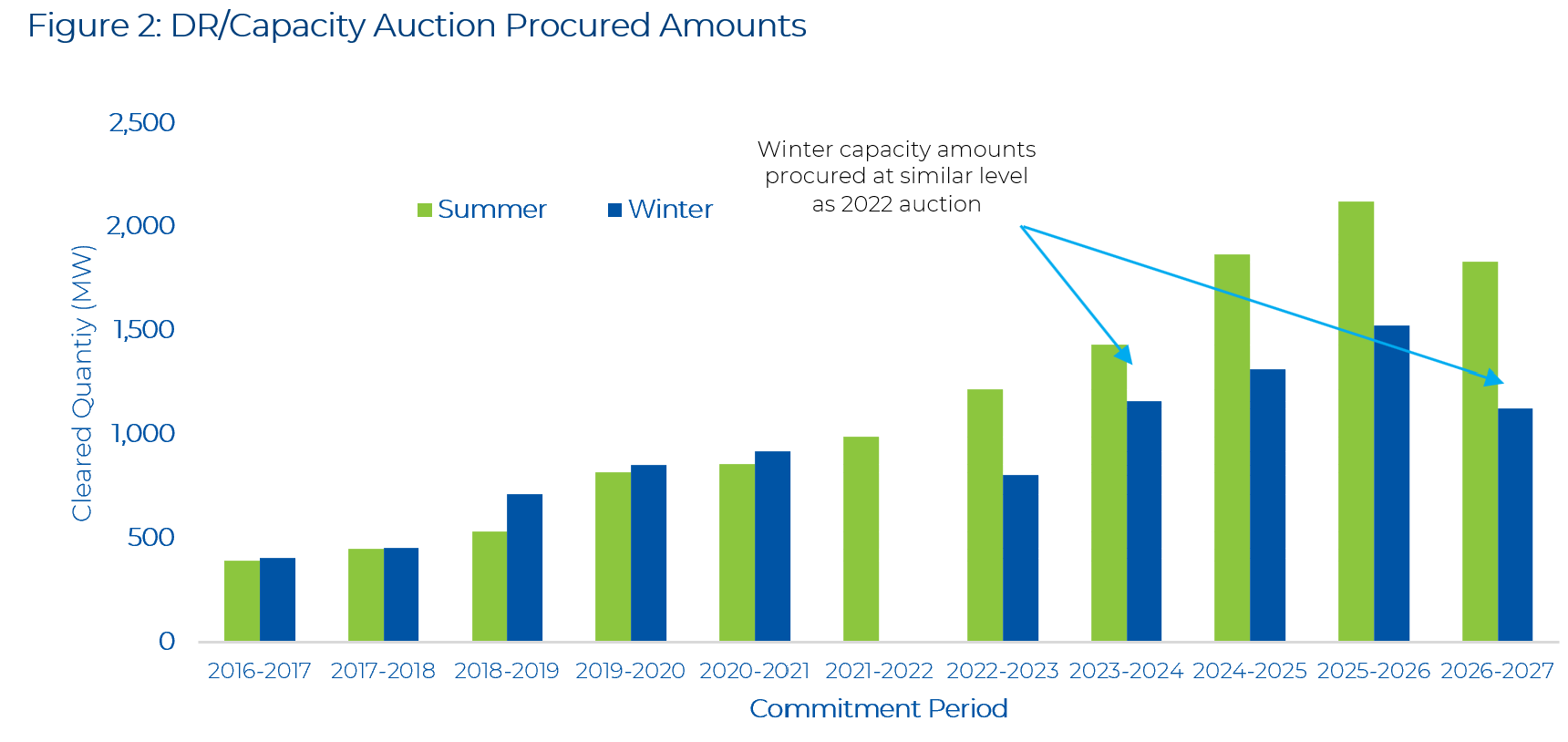

In total, the IESO procured 1,832.8 MW of capacity for the summer of 2026 and 1,125.3 MW for winter of 2026-2027– falling short of the target capacity in the winter. The IESO’s pre-auction targets were 1,800 MW for the summer and 1,200 MW for the winter of 2026-2027. The total capacity amounts procured were also slightly less than the previous auction, even though the targeted amounts were higher. The amount of capacity procured for the winter in this auction was lower than the amount procured in the last three annual auctions.

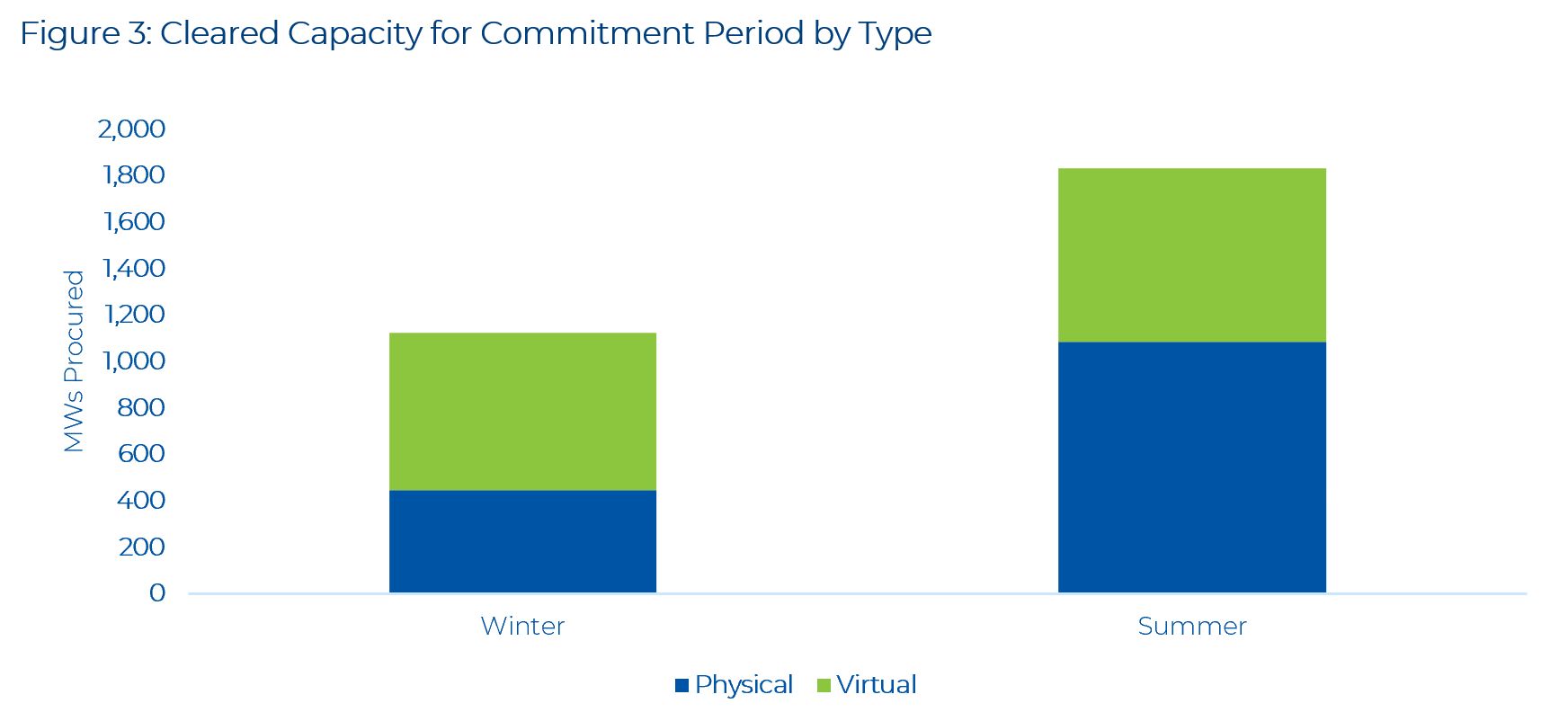

For the winter months, the majority of capacity procured was from virtual resources (i.e. aggregated DR resources which are not metered by the IESO). In contrast, in the summer, physical capacity – which is capacity from single, large resources and imports – were the majority, largely as a result of summer import capacity from Hydro Quebec increasing from 400 MW to 600 MW. Since imports were enabled in 2021, the IESO has steadily increased the cap on capacity eligible from Hydro Quebec, and Hydro Quebec has cleared this full amount in every summer commitment period. In contrast to last year’s auction, no resources from thermal assets in New York were procured.

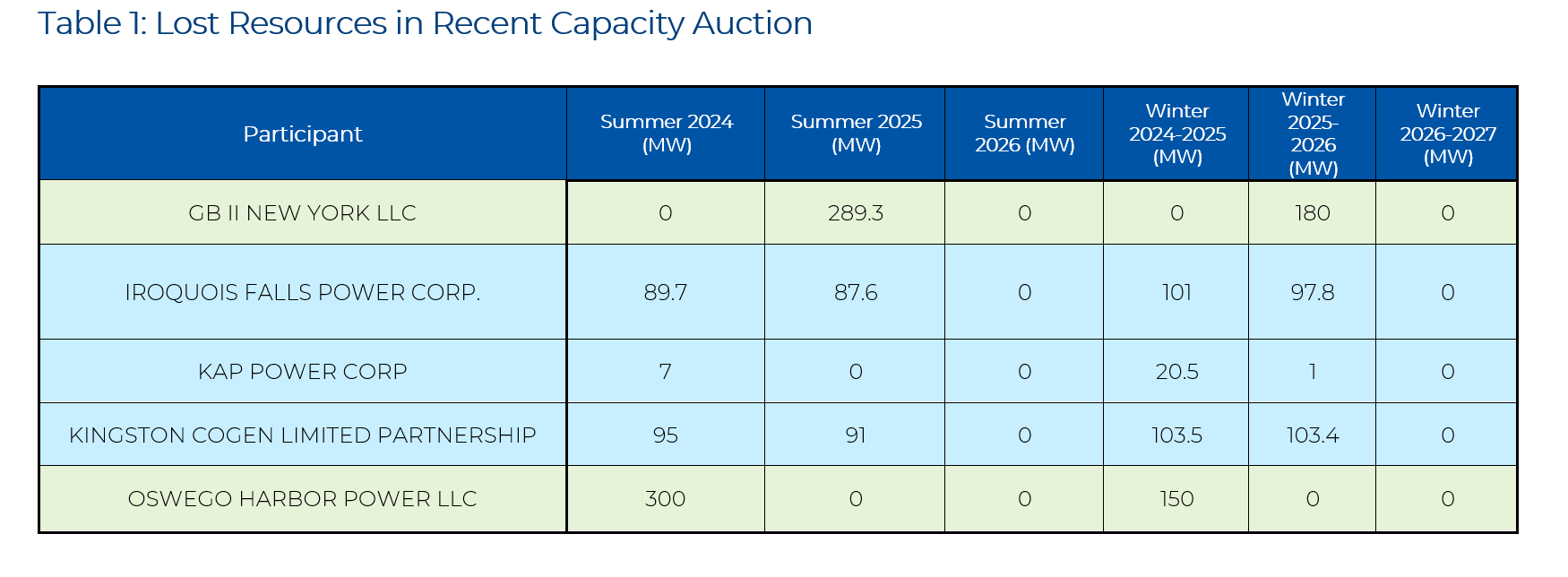

A number of large participants in previous auctions did not receive commitments this time around, including imports from New York (highlighted in green) and a number of thermal assets that secured Medium-Term 2 (MT2) contracts (highlighted in blue) with the IESO. The reduction in summer supply from these resources totalled more than 470 MW. The MT2 prices for most successful generators are below the effective annual Capacity Auction price.

Power Advisory Commentary

The significant increase in capacity prices is important for a number of reasons.

First, and most importantly, it’s another sign of the tightening supply/demand balance that Ontario is now facing. Energy and Operating Reserve (OR) prices – as we have discussed throughout our renewed market commentaries – have been well above historical levels over the past year. We expect energy prices to remain elevated given forecasted demand growth and the retirement of the Pickering Nuclear Generating Station (PNGS), which will remove 2,100 MW of baseload supply at the end of 2026. In short, Ontario’s grid is getting very “tight” and while that first appeared in the energy market, it is now showing up in the capacity market. Rising prices are not necessarily a negative outcome or a result of flawed market design; higher energy and capacity prices serve as a signal of tight supply and an incentive for new supply to enter the market.

Second, year-to-year changes in supply from Ontario-based generation and generator-backed imports can lead to Capacity Auction price volatility. With the removal of a number of thermal assets due to MT2 contracts – i.e. they now have 5-year contracts with the IESO and do not need to participate in the Capacity Auction – there was no replacement of that capacity. Instead, there was an increase in aggregated DR capacity and summer imports from Quebec, but not to the extent to fully offset the lost supply from the gas plants in the Capacity Auction.

Third, the entire eastern part of North America – including Ontario, Quebec, NYISO, PJM, MISO and ISO-NE – is increasingly becoming very tight on capacity. For example, NYISO’s recent 10-year Comprehensive Reliability Plan warned that “New York’s electric system faces an era of profound reliability challenges.” New York is not alone, as Quebec, ISO-NE, MISO and PJM all face high demand growth, aging assets and a struggle to connect enough firm, dispatchable capacity needed to maintain reliability. With that tightening supply/demand balance across such a large region, procuring capacity through the province’s interties will either become challenging from a physical perspective (i.e. the capacity is not available) or expensive, as the opportunity cost of participating in Ontario compared to other jurisdictions is high. The lack of participation from New York-based assets may be the first sign of this challenge.

And finally, participant behaviour in the Capacity Auction may have already changed – recognizing that there was going to be a tight supply/demand balance – and may continue to change going forward. In principle, higher clearing prices should encourage more load customers to offer DR; however, it is not clear how much achievable DR potential remains in Ontario and how quickly new DR supply could enter the market. If there is insufficient new capacity in future auctions, participants may feel comfortable pushing offer prices higher. The unique Class A/B cost allocation design in Ontario may also impact the Capacity Auction. As energy prices move higher, Global Adjustment (GA) costs will decline and the value of the “peak chasing” is reduced. These resources may try and recover some of that reduction in revenue through higher Capacity Auction offer prices.

As we have suggested in numerous different venues and commentaries, Ontario is facing a new reality when it comes to its supply/demand balance and prices. The Capacity Auction prices are the most recent reflection of that change.