This article is an update to a previous article published April 20, 2026

After a winter hibernation in which Pennsylvania solar net metering developers hunkered down and awaited developments on a number of fronts, spring and summer have yielded some market clarity in how net metering projects will likely be treated moving forward. And in a welcome surprise, the value stack of the hourly pricing-based Price to Compare (PTC) that customer-generators will receive moving forward currently offers an attractive return on excess generation.

At present, a massive number of “merchant” net metering projects (those without independent onsite load) are under development but few have gone operational. The first projects to come online were in early 2025. As of November 1, 2025, the Public Utilities Commission (PUC) reported that 23 merchant net metering projects totaling about 58 MW had come online1, most of which were in PPL territory2. The PUC expected that 68 systems would be online by May 31, 2026 (approx. 170 MW). All told, the PUC said that about 2,000 merchant net metering projects totaling 4.5 GW had been reviewed by staff to date.

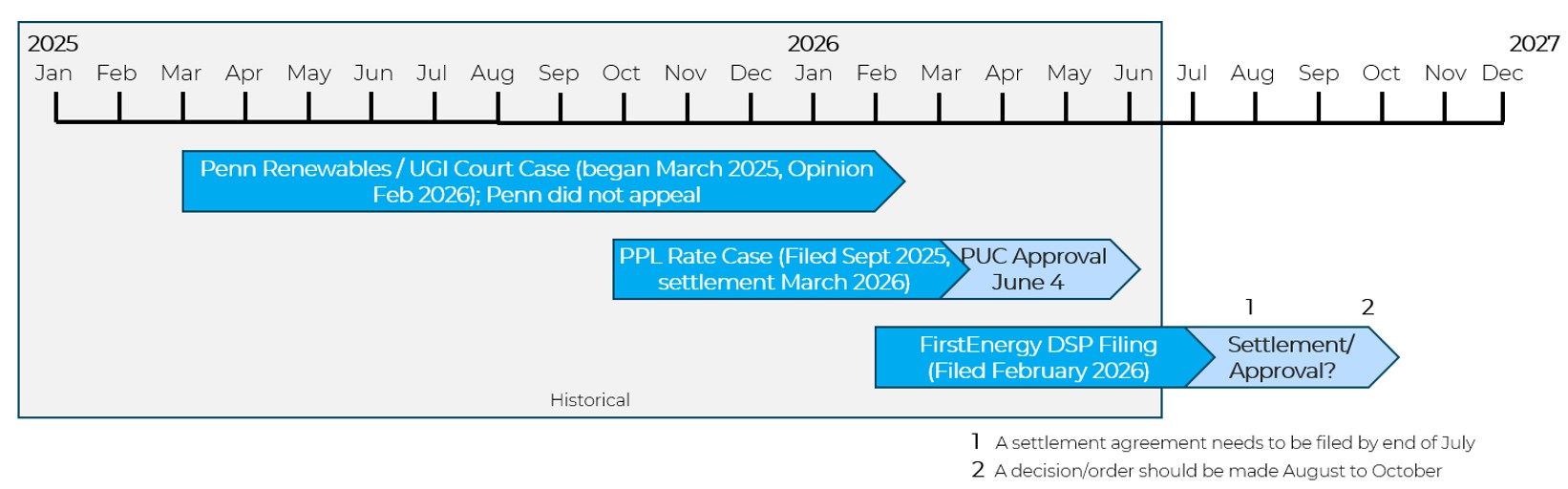

There are several storylines developing in parallel as project developers – and their investors and lenders – assess their next moves. Figure 1 shows the timeline of the key processes that are in play, sorted in chronological order based on when they began.

Figure 1. Pennsylvania Net Metering - Important Timeline

In this article, we provide updates on the following topics that are all driving forces of Pennsylvania net metering projects, which have unfolded in the past several months:

PPL Proposed Settlement

As described in our previous update, PPL Enters the Fray with Rate Case Filing, on September 30, 2025, PPL Electric Utilities (“PPL”) filed a request to increase distribution base rates (under docket no. R-2025-3057164)3. On March 5, 2026, a proposed settlement was published by PPL and the Joint Solar Advocates (JSA), which consisted of industry trade groups Solar Energy Industries Association (SEIA) and the Coalition for Community Solar Access (CCSA)4. The settlement included the following highlights:

a. Customer-generators who submitted to PPL an interconnection application on or before September 30, 2025, which is the date on which PPL filed the rate case, and whose generating facilities either (i) receive a Permission to Operate (PTO), or (ii) provide to PPL Electric a completed copy of their Certificate of Completion on or before December 31, 2026, which is 15 months from the rate case application date; then

b. Customer-generators who submitted to PPL Electric an interconnection application on or before September 30, 2025, up to the cap, based sequentially on the date of their signed original Notification of Customer Intent ("NOCI").

No additional customer-generators would be grandfathered into fixed price default service (GSC-1) under the process once the total amount of nameplate AC capacity for Rate GSC-1 customer-generator systems that receive Permission to Operate (PTO) reaches 140 MWAC.

Thus, the date of the signed original NOCI will determine whether a project is grandfathered or not. At this time, however, project developers would not know where they are in the queue, so it will be some time before the 140 MW allotment is known. Certainly, operating projects will be grandfathered. It’s a matter of which projects currently under construction and earlier will also be grandfathered.

The settlement agreement finally provides some much desired market clarity to developers and investors. Not only that, but it affords a more optimistic value stack than the market had expected, as will be described later on.

While PPL has agreed to not change the structural components between customer-generators and non-customer generators, there is some risk that PPL might adjust how it calculates a given rate component at some point in the future as a means of reducing the realized rate to the net metering customer-generator. While energy and capacity are unlikely to be touched, the way transmission is calculated could be changed. At present, the transmission charge is a very favorable cost component; in fact, it is the largest component of the four components in the PPL value stack. However, this is a double-edged sword for PPL: a change could reduce what it pays to customer-generators, but at the same time, it could reduce the revenue it derives from ratepayers.

The settlement does not explicitly state how long a project would be entitled to net metering credits, but in the absence of any mention, one assumes that it is for the project life. As a reminder, there are no contracts executed by the project owner and utility for net metering in Pennsylvania.

Approval by the PUC of PPL’s rate case and settlement

On June 4, the Pennsylvania PUC approved PPL's rate case and settlement, PUC Issues Decision in PPL Electric Rate Proceeding5. The settlement between PPL and the JSA was approved as filed except that agricultural biogas customer-generators are excluded from the large, "no-load" net metering facilities and reclassification. Thus, there is just one minor change which doesn’t affect solar customer-generators.

Leading up to the PUC approval, a coalition of 17 developers opposed the settlement, focusing their objection on just one issue, the Maximum Registered Peak Load (“MRPL”) provisions which enable the long-term reclassification of net metering projects to the hourly based GSC-2 PTC6. This is not an insignificant coalition in terms of its size, but nonetheless, the PUC did not vote in their favor.

This result – the PUC approval – was largely expected. It now provides more certainty in the Price to Compare (PTC) payout for net metering facilities in PPL.

FirstEnergy Default Service Plan (DSP) Filing

On February 3, 2026, FirstEnergy filed its Default Service Plan (DSP-VII) for the period June 1, 2027-May 31, 20317. Among other things, this plan addresses net metering. During the discovery process of DSP-VII, FirstEnergy has been informing customer-generators how they will be compensated at the PTC under the new DSP. The highlights of DSP-VII and impacts to net metering include:

The DSP is currently in the discovery phase. Direct, rebuttal testimony and cross examination have been ongoing; filing of main briefs or submission of joint settlement petition are scheduled for July/August. The DSP and any settlement agreement, if filed, should be approved in fall 2026. The JSA lawyers (CCSA and SEIA) are actively negotiating with FirstEnergy as regards net metering.

As is shown later on, the value stacks of the FirstEnergy companies in the HP Rider are lower than PPL’s hourly-based PTC.

Penn Renewables v PUC Decision

Following the PUC’s approval of UGI’s default service plan that included the rate reclassification placing customer-generators into its hourly Locational Marginal Pricing (LMP) GSR-2, Penn Renewables LLC (“Penn Renewables”), a renewable energy developer,filed an appeal in the Pennsylvania court system in March 20258. In March 2026, the original order was affirmed by the court9. Penn Renewables did not appeal the decision, and thus, the reclassification of customers by using their “supply peak load impact” (the equivalent of MRPL) will remain effective. This likely means that PPL, FirstEnergy and other utilities will be permitted by law to use the MRPL to classify customer-generators once approved by the PUC. All net metering projects moving forward can expect to be classified in the hourly-based PTC if not included in a utility’s grandfathering.

PTC Value Stacks – Retail and Hourly-Based

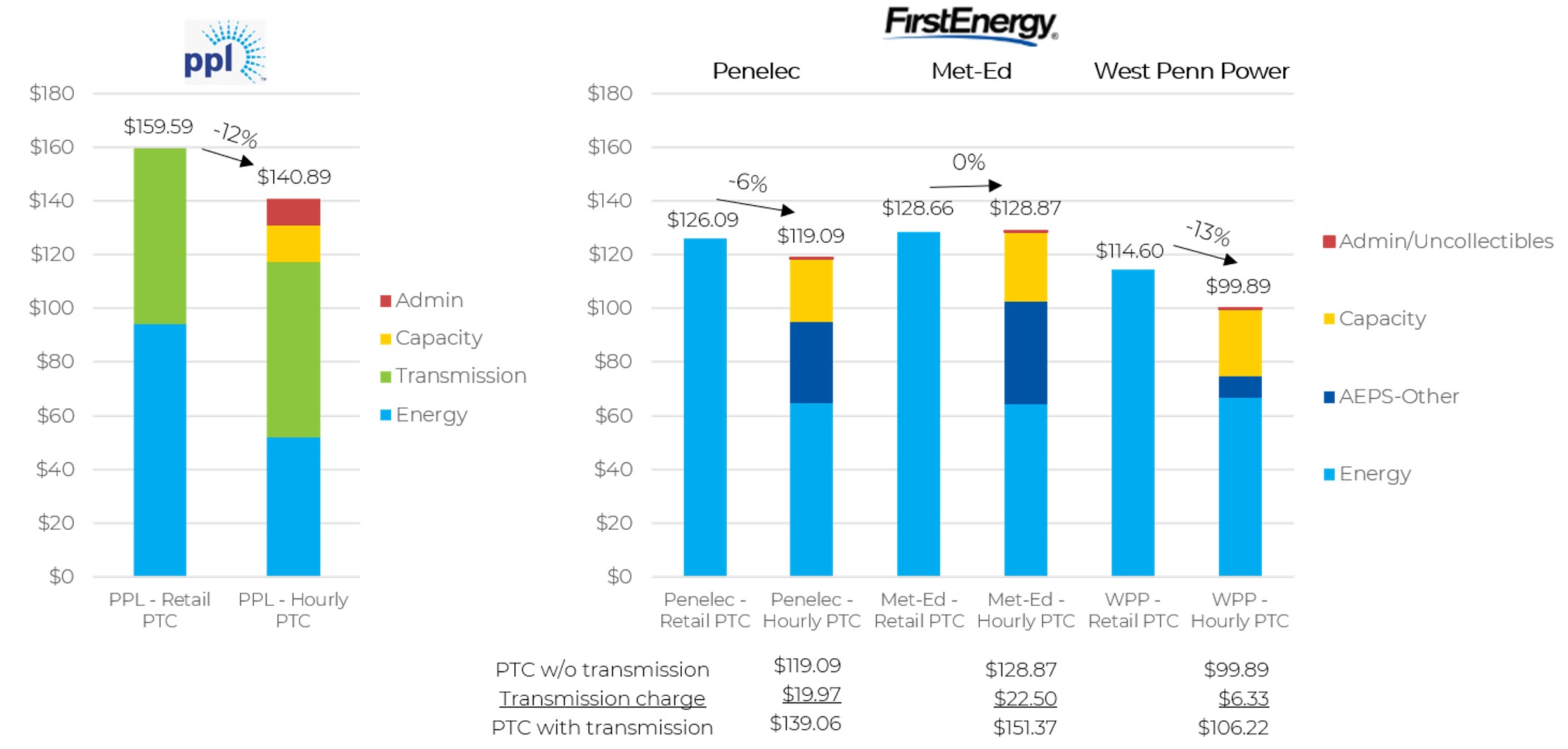

With the transition from retail to hourly-based PTC rates, market participants have turned their attention to the hourly-based value stacks. And the news is not bad. For PPL, the retail PTC for 2026 is estimated to be $159.59/MWh while the hourly based PTC is estimated to be $140.89/MWh, a 12% decline; see Figure 2 for 2026 average annual value stacks. Note that there are published rates through November 2026 for some rate components (but not the LMP). For FirstEnergy utilities, the comparison of the retail PTC to hourly is mixed. If we assume the transmission charge is not included, the Penelec value stack declines by 6%, Met-Ed is flat (0%) and West Penn Power declines by 13% from the retail to hourly PTC. With the transmission charge, Penelec and Met-Ed both increase, while West Penn Power still declines, though only marginally.

Figure 2. Net Metering Credit Value Stack for PPL and FirstEnergy Companies, 2026 ($/MWh)

Note: Some charges have not been filed in a proposed or effective tariff and thus are estimates by Power Advisory. This included PPL’s capacity charge and FirstEnergy’s Transmission charge. In addition, Power Advisory splits the established FirstEnergy Cap-AEPS-Other charge into a capacity value and AEPS-Other value.

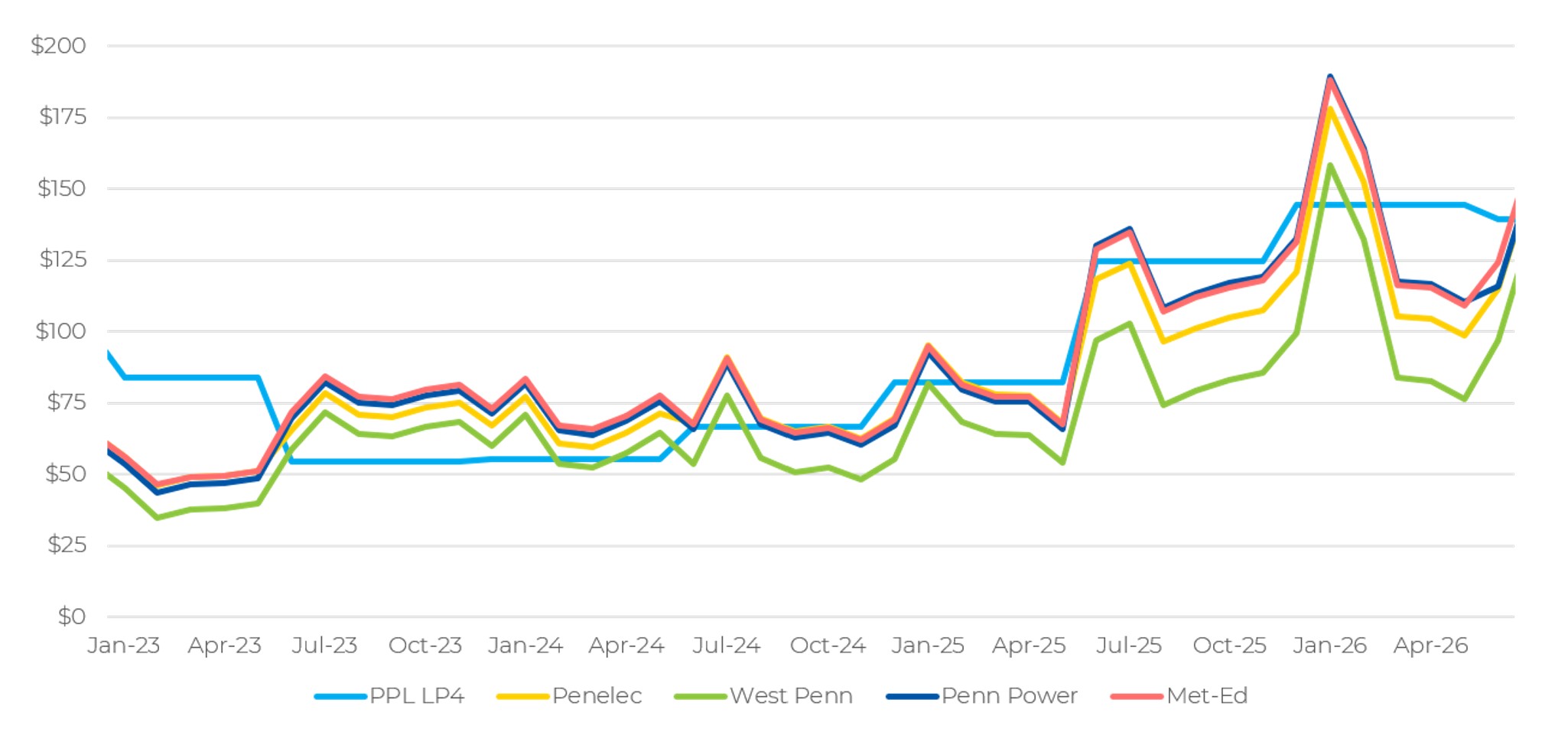

Figure 3 shows the historical monthly hourly-based PTCs for five Pennsylvania utilities. The rates in May 2026 ranged from $76/MWh for West Penn to $144/MWh for PPL. One can see the volatility for FirstEnergy PTCs as compared to PPL because the FirstEnergy HP Rider utilizes the LMP matched with the hourly production of a net metering facility (solar weighted). And there is significant variation of monthly PTC values within a given year. In 2023, the total hourly PTCs ranged between $35/MWh and $85/MWh, and in 2026 so far, the total hourly PTCs have been between $76/MWh and $190/MWh. On average, these rates increased from $59.10/MWh in Jan 2023 to $107.73/MWh in May 2026, an 82% increase. This remarkable increase in rates can make the net metering projects receiving hourly-based PTCs economic today.

Figure 3. Historical Hourly-Based Price-to-Compare (PTC) Rates, Jan 2023-June 2026 ($/MWh)

Figure 4 shows the breakdown of rate components for PPL’s hourly PTC. As can be seen, for the current month (May 2026), the transmission charge is the highest charge, followed by the hourly LMP. The capacity charge is third, and administrative charge, fourth. While these last two charges are much smaller than the first two, they have nonetheless increased materially in the recent past.

Figure 4. Historical PPL GSC-2, Jan 2022-May 2026 ($/MWh)

A good portion of the credit is the hourly LMP. PPL, as agreed in the Settlement Agreement, will use a 6-month average of LMPs, aligning with the current supply periods (June-Nov & Dec-May) to calculate the LMP energy component. The significantly higher December 2025 – February 2026 LMP values seen in PJM have increased the recent value of the hourly-based PTCs. There is inherent risk relying on wholesale market prices as a major component of the PTC. The hourly-based PTC can exhibit vastly difference total values depending on whether PJM exhibits a high or low priced month or 6-month period. At present, the futures market is showing that LMPs will remain at current high levels, with seasonal variation. And in the long term, Power Advisory forecasts that energy prices will trend higher than in recent years given the crunched supply and significant load growth expected.

The transmission charge, or NITS charge, is substantial in the PPL PTC value stack. As described earlier, there is risk that PPL alters the structure of the transmission charge reducing its value. But it is two sided with respect to the revenue it earns from load customers. Pennsylvania and PJM at large are expecting significant transmission investment on the grid. As a result, transmission charges should only increase moving forward.

As discussed earlier, for FirstEnergy, we are still awaiting further clarity on whether the NITS charge will be included or not. The expectation at this point is that it will not be included. If it is included, Power Advisory estimates it to be modest, ranging from $6/MWh to $23/MWh across the four utilities.

REC Prices Holding Steady at $22-$25/REC

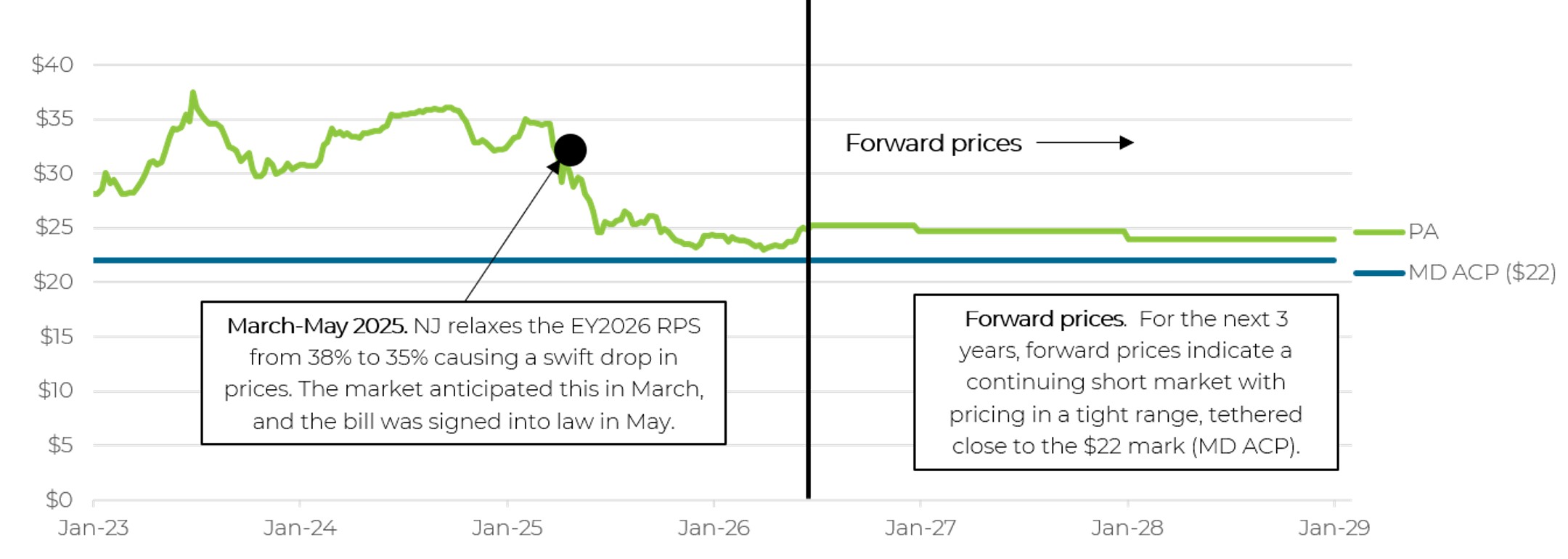

In addition to the net metering credit, a customer-generator will also produce an Alternative Energy Credit (AEC), or REC. These RECs are eligible to sell into the Pennsylvania Tier 1 REC market (technically they can sell into the SREC program as well, but that market is roughly the same price as the Tier 1 market). That market has trended downward from the $30s in recent years into the $22-$25/REC range (Figure 5). Forward markets indicate that prices are expected to remain steady in that range for the next 3-4 years. It continues to be an undersupplied market with prices near the Maryland ACP ($22.25), which acts as a tether for the PJM Tier 1 REC markets (PA, MD, NJ, VA, and DC).

Figure 5. Pennsylvania Tier 1 REC Prices, 2023A-2028E ($/REC)

Proposed Legislation and Risks to Net Metering

There are a number of bills that could potentially impact net metering. Among them, House Bill 2348 would revert net metering to a pre-Hommrich period where customer-generators must have load independent from the alternative energy system and are limited to selling no more than 200% of their onsite load to the grid. There are exceptions for warehouse or commercial rooftop and safe harboring is offered for existing net metering systems (and those with interconnection applications), but the bill would overhaul the Pennsylvania net metering landscape eliminating pure play customer-generators. There is also House Bill 504 which would introduce a community energy facility program, effectively offering a community solar program to similarly-sized projects participating in net metering. The community energy bill credit would be of similar value to the PTC, based on residential and small C&I rates. However, HB 504 has stalled in the Senate, similar to past community solar bills. Finally, the PUC’s position on net metering is quite strong10. The PUC recommends that legislation be introduced to limit the number of megawatts that can participate in net metering at current compensation levels. Many legislators have taken notice of the issue. The House Energy Committee, for example, held a hearing to understand the situation and there have been previous bills other than HB 2348 proposing to limit net metering.

All that said, virtually no new energy legislation has been passed in Pennsylvania in the past 5 years. This is because of partisan gridlock within the Pennsylvania General Assembly, especially pertaining to energy policy. Within parties there are different camps that want different things. The state has yet to see a majority of legislators and the Governor come together and move bills through to completion and into law. Power Advisory believes that none of the described current bills that have been introduced will be made into law.

What’s Next

The net metering market has more certainty than it did eight months ago. While M&A and lending transactions all but shut down following the PPL filing in September 2025, the market has been digesting the recent news, and M&A, along with project development, is resuming. More projects are slated to begin construction. Another immediate consideration for developers – and go/no go decision point – is ensuring that they capture the federal ITC before it is no longer available. That means either safe harboring their project before July 4, 2026, in which case they need to bring the project online no later than December 31, 2030, or placing it in service by December 31, 2027.

Some lenders have shied away from this market because rates are moving from a retail rate to a wholesale hourly-based rate. Though some may reconsider their position given how rates have gone up considerably in the last 2 years. The total hourly-based PTC value stack is not as much of a haircut from retail as originally thought, and depending on the LMP for a given month, it could be an increase. Wholesale energy pricing can alter the story significantly, potentially lowering the PTC value, but forward markets point to higher LMPs over the next five years. It will be important for market participants to stay up to date on the latest values of the PTC stack given the evolving policy environment and wholesale market changes. Specifically, the FirstEnergy DSP-VII and what the full HP Rider PTC value will include should be finalized by end of 2026.

We expect increased activity – both on the M&A front and in terms of developers moving forward with their projects into construction. It’s already happening. All that being said, net metering does face two notable risks: (1) it’s based on a rate that floats rather than a fixed rate, and (2) it’s not a contract, which tends to be more iron clad. Nonetheless, the value of the projects is coming into greater focus and that value, as far as we can tell, makes many projects economic.

We will continue to track and report on developments in this market.

Andrew Kinross, Director, can be reached at akinross@poweradvisoryllc.com.

Andrew Bracken, Manager, can be reached at abracken@poweradvisoryll.com.

Footnotes

1 Compliance for Reporting Year 2024-2025, Pennsylvania Public Utility Commission in cooperation with the PA Department of Environmental Protection, pages 44-46, February 2026. https://www.puc.pa.gov/media/3805/aeps-2025-report_2-5-25_final_.pdf

2 Based on data from the listing of 2-3 MW-ac solar projects that are operational from the PUC. https://pennaeps.com/reports/

3 PPL Electric Utilities Corporation, Docket No. R-2025-3057164, “PPL Electric Utilities Corporation filed Original Tariff No. 202 which is a general rate increase effective December 1, 2025.”, 2025, August 29. https://www.puc.pa.gov/docket/R-2025-3057164

4 Joint Stipulation and Settlement of PPL Electric Utilities Corporation and the Joint Solar Advocates, March 5, 2026, https://www.puc.pa.gov/pcdocs/1916971.pdf; Joint Petition for Non-Unanimous Settlement of All Issues, March 13, 2026, https://www.puc.pa.gov/pcdocs/1918030.pdf

5 Pennsylvania Public Utilities Commission, PUC Issues Decision in PPL Electric Rate Proceeding, June 4, 2026, https://www.puc.pa.gov/...-rate-proceeding-06042026

6 Customer-Generator Coalition, Docket Nos. R-2025-3057164, Objections to the Joint Petition for Approval of Non-Unanimous Settlement, https://www.puc.pa.gov/pcdocs/1920329.pdf

7 FirstEnergy Default Service Plan (DSP) for June 1, 2027-May 31, 2031, Docket No. P-2026-3060298, https://www.firstenergycorp.com/.../PA/tariffs/PA-DSP.pdf

8 Commonwealth Court of Pennsylvania at Docket No. 337 CD 2025

9 Memorandum Opinion, Penn Renewables, LLC v Pennsylvania Public Utility Commission, https://www.pacourts.us/assets/.../337CD25ORD_5-26-26.pdf?cb=1

10 In the PUC’s 2025 AEPS report, it recommends – in forceful terms – that legislation should be introduced that limits net metering program so that it doesn’t cause economic harm to ratepayers. Or that note, the PUC itself recommends reasonable bounds. It says: “The Commission recommends that the General Assembly consider modifying the structure of net metering by placing reasonable bounds on net metering to curb the economic harms of subsidizing excessive wholesale generation that the EDCs are obligated to purchase at retail, rather than at wholesale rates. Alternatively, the General Assembly could authorize the Commission to evaluate and create those reasonable bounds. The need is immediate to avoid harm to the default service market product for small commercial and industrial customers.”